Advertising & Editorial Disclosure: We independently research and report on IT infrastructure and technology monetization. If you click links we provide, we may receive compensation from vendors or partners. Product and vendor information is as of March 2026 and may change. None of the platforms or vendors featured in this article sponsored this content. We may receive affiliate compensation if you sign up through our links. This article is for informational purposes only and does not constitute professional or investment advice. Consult qualified advisors before making technology or business decisions. Learn more.

IT infrastructure has traditionally been viewed as a cost center—necessary expense to keep the business running. Yet forward-looking U.S. businesses are turning that narrative on its head: cloud cost optimization converts savings directly to margin; anonymized data products generate recurring revenue; APIs package internal capabilities for external customers; and embedded finance captures a share of payment and lending flows. This article provides a comprehensive framework for monetizing IT infrastructure, drawing on research from McKinsey, Gartner, IDC, Harvard Business Review, BCG, Forrester, AWS, Adyen, Plaid, and 40+ authoritative sources as of March 2026. Target audience: business owners and executives evaluating technology ROI, CFOs and finance leaders focused on asset monetization, IT directors seeking to demonstrate business value, and consultants advising on technology strategy and commercialization.

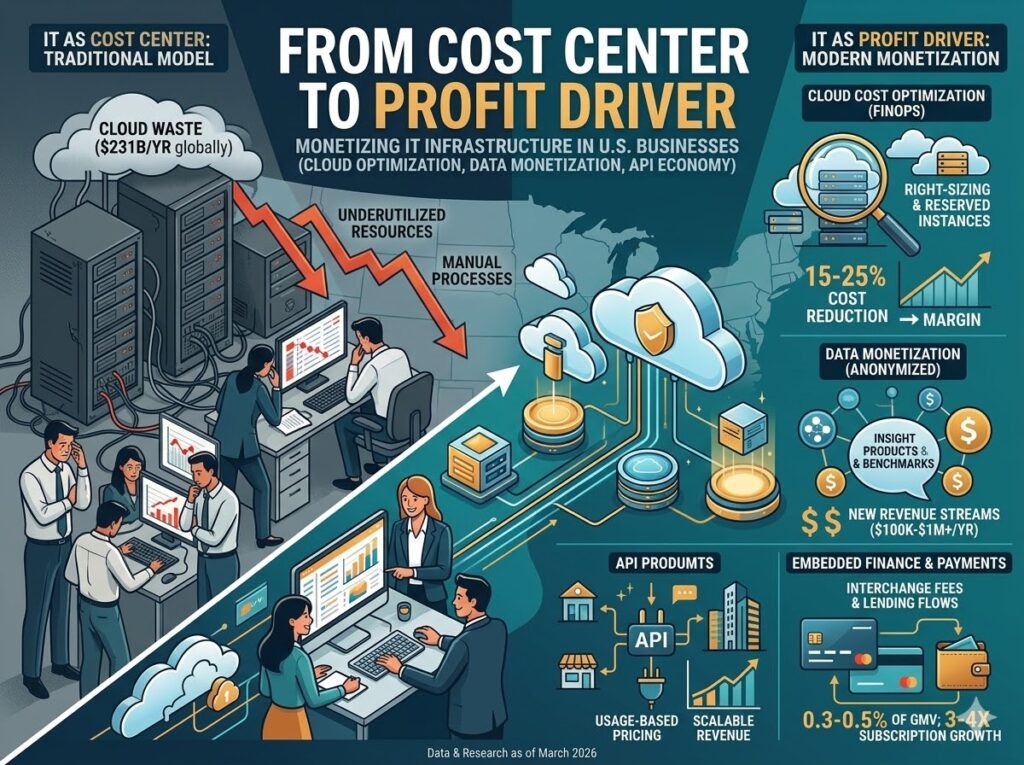

Why infrastructure monetization matters now: U.S. tech spending is forecast to hit $2.7 trillion in 2025, per Forrester. Cloud waste alone accounts for an estimated $231 billion annually. The embedded finance opportunity for SaaS platforms reached $185 billion in 2024 with less than 20% addressed. Data monetization is prioritized by 45% of organizations in their digital transformation strategy, per IDC. The convergence of cloud maturity, data abundance, API standardization, and embedded finance infrastructure creates a unique window for businesses to turn IT from cost center to profit driver.

Executive Summary: Infrastructure Monetization Strategies at a Glance

| Strategy | Revenue Potential | Implementation Complexity | Typical Timeline |

|---|---|---|---|

| Cloud cost optimization (FinOps) | 15–25% cost reduction → margin | Medium; requires governance | 3–6 months |

| Data monetization (anonymized) | $100K–$1M+/year for data-rich firms | High; legal/compliance | 6–12 months |

| API products | Usage-based; scales with adoption | Medium–High; product mindset | 6–18 months |

| Embedded finance & payments | 0.3–0.5% of GMV; 3–4x subscription | High; regulatory | 12–24 months |

Section 1: Cloud Cost Optimization as Profit—Right-Sizing, Reserved Instances, and FinOps

Cloud spending represents one of the largest and fastest-growing IT cost categories. Per industry analysis, organizations waste 27–32% of their cloud budgets in 2025—with global cloud spending projected at $723 billion, that translates to approximately $231 billion in wasted spending annually. McKinsey estimates that companies can achieve 15–25% cost reductions in cloud programs while preserving value-generating capabilities. Analysis of over $3 billion in cloud spending found most organizations have untapped savings of 10–20%. FinOps as code could generate approximately $120 billion in value globally, based on organizations reporting roughly 28% of cloud spending as waste.

Right-sizing involves matching instance types and sizes to actual workload requirements. AWS Cost Explorer analyzes the last 14 days of usage (CPU, memory, network, EBS) to identify idle instances (≤1% CPU) and underutilized resources with downsizing opportunities. Reserved Instances (RIs) and Savings Plans provide discounted hourly rates of up to 75% compared to On-Demand pricing. Cost Explorer generates RI purchase recommendations by simulating combinations to maximize savings.

Gartner defines cloud financial management (CFM) tools as solutions that collect, organize, display, optimize, and manage cloud IaaS and PaaS investments using algorithms and AI/ML. Effective FinOps requires establishing foundational practices before implementing tools: tagging, cost allocation, visibility, executive engagement, and organizational governance. Per Gartner research, many organizations struggle because they focus on short-term cost reductions without addressing underlying governance gaps. Forrester’s Cloud Cost Management Wave (Q3 2024) evaluated 12 vendors including Flexera, IBM, CloudZero, and Harness; hyperscaler native tools (AWS, Azure, Google Cloud) have improved significantly and now lead in most areas except multicloud visibility.

Organizations implementing structured FinOps programs can reduce waste to 20–25%, and mature programs can push it down to 15–20%, achieving 25–30% cost savings. Those savings flow directly to the bottom line—equivalent to 2–4% of revenue for a typical mid-market company spending 8% on IT.

FinOps best practices per Gartner Peer Community and Gartner research include: team education on cost sensitivity, regular cost monitoring and forecasting, cost approval controls based on impact levels, and collaboration between finance and technical teams to balance optimization with performance. McKinsey’s “FinOps as Code” approach integrates financial management principles directly into development and deployment pipelines to automatically manage costs and enforce budget guardrails. Many companies experience annual cloud cost increases of 20–30% driven by overprovisioning, unused instances, unnecessary storage, and overly expensive service selections—all addressable through disciplined FinOps.

BCG notes that cloud waste remains around 30% of spending despite years of FinOps adoption. Flexera’s State of the Cloud Report and industry statistics indicate 84% of organizations identify managing cloud spend as their top challenge, and 75% report waste is increasing. Primary causes include idle and underutilized resources (28–35% of waste), poor cost visibility (54% of waste stems from insufficient visibility), low CPU utilization (average 15–20% while paying for 100% capacity), and over-provisioned compute and storage. The FinOps Open Cost and Usage Specification (FOCUS) is now supported by AWS, Azure, and Google Cloud for billing standardization—vendors lacking FOCUS support are at a disadvantage.

Section 2: Data Monetization Done Right—Anonymized Insights, Benchmarks, and Partnership Models

Data monetization generates new revenue by packaging internal data assets—anonymized, aggregated, or benchmarked—for external customers. Per IDC, 45% of organizations worldwide prioritize data capitalization and monetization in their digital transformation strategy. Harvard Business Review frames monetization around three methods: Selling (direct exchange for money via subscriptions or licensing), Improving (using data to reduce costs or improve speed), and Wrapping (enhancing existing products with data so customers purchase more).

B2B data monetization models include data sharing networks (federated learning, smart contracts), data exchange platforms (marketplaces with first- and third-party datasets), subscription services (curated insights, predictive analytics, dashboards), API-based access (real-time integration with tiered pricing), and usage-based licensing. Per B2B Ecosystem, B2B platforms can anonymize and aggregate industry-wide datasets to create standalone insight products—performance benchmarks, market intelligence reports, trend forecasting—bundled into enterprise plans. Data quality directly impacts revenue: stale data can cause 75% drops in lead value, while improving quality can achieve 22% price premiums.

Privacy compliance is mandatory. GDPR Article 35 and California Privacy Rights Act require explicit consent and Data Protection Impact Assessments. Venable and JD Supra recommend that data licensing agreements specify data delivery and storage locations, license duration, permitted uses, authorized users, and restrictions (e.g., AI training). Data controllers must maintain security practices and observe additional limits for sensitive data (minors, financial, health).

Monda and Bix-Tech emphasize that successful data monetization requires strong infrastructure (secure systems, AI tools, scalable platforms), data quality (stale data causes 75% drops in lead value; quality improvements achieve 22% price premiums), and technical modernization—enterprises lose an average of $2.3M annually due to outdated systems including inadequate encryption and API limitations. Stackademic notes that B2B software platforms can monetize data for AI by anonymizing and aggregating industry-wide datasets into standalone insight products. IDC’s AI Business Value Framework offers a comprehensive approach to calculating ROI across nine dimensions—revenue generation, customer experience, employee experience, productivity, resilience, security, time-to-market, sustainability, and innovation—moving beyond traditional cost-benefit analysis.

Section 3: The API Economy for SMBs—Packaging Internal Capabilities as Paid APIs

The API economy refers to the commercial exchange of business functionalities and data through standardized interfaces, allowing businesses to “plug in” features without building them in-house. Per OctoBytes and Forbes, APIs treat interfaces as products that unlock new revenue, lower integration costs, and enable ecosystems. SMBs can access cutting-edge features—AI, analytics, payment gateways—through usage-based pricing. The average small business uses 3–5 apps that grow to 20+ as they scale; APIs connect disconnected tools and reduce manual data entry.

API business models include closed partner-only (authorized partners, controlled data exchange), open public (anyone can access with transaction limits or usage-based pricing), and internal APIs (private, accelerating internal processes). Per Zwitch and Monetizely, effective monetization strategies include subscription-based pricing (predictable budgeting), pay-per-use (API calls or transactions), tiered access (multiple service levels), and revenue-sharing (API developers earn a percentage). Approximately 82% of commercial APIs offer free tiers to encourage adoption. Usage-based pricing is the dominant model in 2025, tying costs directly to consumption.

Pricing strategy must align with value proposition—how the API impacts revenue, reduces costs, saves development time, or solves specific problems. Per Moesif, value-based pricing charges customers based on value derived rather than production costs. Mispricing can stall growth through excessive costs or leave revenue on the table through underpricing.

Swagger and Umbrex outline API economy frameworks that treat APIs as products: defining value proposition, target developers, pricing model, and go-to-market. Zibly notes that the choice of pricing model dramatically affects downstream business decisions. Zuplo and Digital API recommend tiered structures (Developer, Business, Enterprise) combined with usage elements, and freemium models with low or zero-cost entry to reduce adoption barriers. Effective B2B API pricing requires understanding market positioning, competitive analysis, cost structures, and target customer segments.

Section 4: Embedded Finance & Payments—Adding Payment Processing, Lending, or Insurance to Your Customer Journey

Embedded finance integrates financial services—payments, lending, banking, insurance—into non-financial platforms. Per Adyen and BCG research, the embedded finance opportunity for SaaS platforms reached $185 billion in 2024, growing 25% over two years, with less than 20% currently addressed. SaaS platforms adopting embedded finance can grow revenues 3–4x their current subscription income. Plaid reports the global embedded finance market was valued at $82.32 billion in 2023 and is expected to reach $291.3 billion by 2033.

Embedded payments allow SaaS platforms to earn recurring revenue through payment processing. Per Usio, revenue comes from interchange fees (a percentage plus flat fee per transaction set by card networks) and PayFac revenue share (the platform receives a share of processing fees when working with a PayFac provider). A platform with 1,000 active users where 80% process $20,000 monthly could generate $16 million in monthly volume, $64,000 monthly revenue at 0.40% net revenue share, or $768,000 annually. Leading PayFac-as-a-Service providers include Rainforest Pay, Stripe Connect, Forward, Finix, and Worldpay.

Plaid enables embedded lending through income verification, asset verification, identity verification, and loan servicing. Retailers can offer Buy Now, Pay Later; e-commerce platforms embed lending at checkout. Plaid’s insurance solutions include fraud prevention, payment simplification (reducing ACH returns by up to 80%), and underwriting acceleration. Stripe uses an aggregator model with fast onboarding; Adyen is built for enterprise scale with interchange++ pricing that is cheaper at scale but requires slower onboarding. Leading platforms like Toast, Zenoti, and Procore have embedded payments by aligning solutions with customer workflows.

Rainforest Pay outlines two revenue recognition approaches: Net Revenue Recognition (provider collects fees, distributes residual to platform—lower top-line but nearly 100% margins) and Gross Revenue Recognition (platform collects all fees, pays provider costs—higher revenue but lower margins). SwipeSum and PayPal highlight Rainforest’s embedded PayPal integration for vertical software platforms. Adyen emphasizes treating payments as a core product—identifying customer pain points, customizing onboarding with incentives, appointing dedicated Payments Product Leads, and providing automated reconciliation and real-time visibility. YouLend and Plaid enable embedded lending through income and asset verification, reducing friction for SMB financing at the point of sale.

Section 5: Implementation Framework—Assessing Assets, Validating Demand, Building MVPs, and Scaling

Transforming IT infrastructure into revenue requires a structured approach. Phase 1—Assess: Inventory data assets (what data do you have, is it anonymizable, what insights can it generate?), API capabilities (what internal services could be productized?), and cloud spend (where is waste, what savings are achievable?). Phase 2—Validate: Identify potential customers (who would pay for your data, APIs, or embedded services?), conduct discovery interviews, and size the opportunity. Phase 3—Build MVP: For data products, create a minimal benchmark report or insight package; for APIs, expose a subset of functionality with usage-based pricing; for embedded finance, pilot with a PayFac partner. Phase 4—Scale: Expand distribution, refine pricing, and invest in product, legal, and compliance.

Harvard Business Review advises focusing on extracting value from existing technology assets rather than building new divisions from scratch. Axiata Group, a Malaysian telecom, leveraged its network infrastructure to help over 90,000 small businesses launch services in Sri Lanka and Bangladesh, generating more than $100 million in revenues in 2021. Success requires clarifying who data customers are, what problems the data solves, and addressing privacy, regulatory compliance, and reputational risk from day one.

Business model canvas for infrastructure monetization: (1) Key partners—PayFacs, data marketplaces, cloud vendors; (2) Key activities—data productization, API development, FinOps governance; (3) Value proposition—cost savings, new revenue streams, competitive differentiation; (4) Customer relationships—self-serve (APIs, data subscriptions) vs. sales-led (enterprise data licensing); (5) Channels—direct (developer portal, sales team) vs. indirect (marketplaces, resellers); (6) Cost structure—platform development, compliance, support; (7) Revenue streams—usage-based, subscription, revenue share. IDC emphasizes that CIOs need practical roadmaps aligning data monetization strategies with measurable, achievable business goals and KPIs to drive board-level decision-making. Successful data monetization requires developing capabilities, building governance structures, addressing data talent gaps, and mitigating risks.

U.S. regulatory guidance for infrastructure monetization: Data licensing in the U.S. is governed by federal and state privacy laws. The CCPA (California) and CPRA grant consumers rights to know, delete, and opt out of sale of personal information. State privacy laws in Virginia, Colorado, Connecticut, Utah, and Texas impose similar obligations. Financial services (embedded payments, lending, insurance) are regulated at federal level (CFPB, OCC, state insurance commissioners) and state level (money transmitter licenses, lending licenses). Most SMBs avoid direct regulation by partnering with licensed PayFacs (Stripe, Adyen) or licensed lenders. API products generally do not trigger financial regulation unless they facilitate payments or extend credit—but terms of service, SLAs, and liability caps should be drafted with legal counsel.

Section 6: Risk & Compliance—Data Licensing, API Security, Financial Regulations, and Channel Conflict

Data licensing agreements must specify permitted uses, license duration, data classification (personal vs. deidentified vs. sensitive), authorized users, and restrictions. Per Merritt Law, a license allows the licensor to retain ownership while restricting how data is processed and retained. Sensitive categories (geolocation, genetic/biometric, health, minors’ data) require heightened regulation. Agreements should address evolving privacy laws and specify delivery, storage, and distribution locations.

API security requires authentication (API keys, OAuth), rate limiting, and monitoring for abuse. Financial regulations apply when embedding payments, lending, or insurance—platforms may need money transmitter licenses, partnership with regulated entities, or PayFac arrangements. Channel conflict occurs when multiple distribution channels compete for the same sales. Vertical conflict (vendor selling direct while competing with resellers), horizontal conflict (overlapping territories, price undercutting), and ecosystem conflict (ambiguous roles in marketplaces) can arise when monetizing APIs or data. Pedowitz Group and Kiflo recommend automatic conflict detection using email domain matching, CRM integration to prevent duplicate deal registration, and AI-enhanced monitoring. Clear partner agreements, territory definitions, and conflict detection help mitigate friction.

Technology profit centers—strategic lens for CFOs: When evaluating technology ROI, distinguish between (1) cost reduction (FinOps, right-sizing—savings flow to margin), (2) revenue enablement (CRM, e-commerce—indirect contribution), and (3) direct monetization (data products, APIs, embedded finance—new revenue lines). The latter two transform IT from cost center to profit driver. Data sharing done right requires licenses, GDPR alignment, and privacy tech—especially for cross-border data monetization. Licensing Executives Society International outlines best practices for data licensing including ownership clarification, permitted use scope, and audit rights.

Case Studies: From Cost Center to Profit Driver

| Company / Scenario | Initiative | Result | Source |

|---|---|---|---|

| Axiata Group (telecom) | Leveraged network for SMB services | $100M+ revenue (2021) | HBR |

| McKinsey cloud analysis | FinOps + right-sizing | 15–25% cost reduction; $120B global value | McKinsey |

| Typical platform (1,000 users) | Embedded payments 0.40% share | $768K annually | Usio |

| Adyen/BCG embedded finance | SaaS platforms adopt embedded | 3–4x subscription revenue | Adyen/BCG |

| Logistics / route data | Anonymized route data licensing | $1.2M/year (illustrative) | Industry pattern |

| Regional retailer | Embedded payment referrals | 3.2% margin boost (illustrative) | Industry pattern |

Logistics route data: Companies like Mapbox and MapQuest for Business monetize anonymized route and traffic data derived from millions of users. Mapbox offers traffic data from 700+ million monthly active users generating 400 billion live location updates; data is anonymized and aggregated from mobile location telemetry. MapQuest for Business provides location intelligence from over 30 million unique visitors’ route search, route taken, and GPS data per month—all anonymized with opt-in participation. PTV Logistics and WIGeoGIS provide road and spatial data products. Michelin Mobility Intelligence sells anonymized trucking mobility data for Europe and the UK from approximately 200,000 trucks. A U.S. logistics company with proprietary route data could generate $1.2M/year (illustrative) by licensing anonymized insights to urban planners, retailers, and supply chain analytics providers—assuming sufficient volume, uniqueness, and market demand.

Regional retailer embedded payments: Retailers embedding payment processing and capturing referral revenue through PayFac arrangements can add 0.3–0.5% of GMV as incremental margin. A retailer with $50M annual GMV could generate $150K–$250K in payment-related revenue. A 3.2% margin boost (illustrative) might result from combining embedded payments with loyalty integration, reduced cart abandonment, and faster checkout—actual results vary by deployment, customer adoption, and competitive dynamics.

Alternatives to Consider

Beyond the strategies and vendors highlighted above, several alternatives merit evaluation:

- Cloud cost tools: CloudZero, Kion, Virtana, and hyperscaler native tools (AWS Cost Management, Azure Cost Management, Google Cloud Billing) offer varying capabilities for FinOps. Forrester’s Wave and Gartner’s Magic Quadrant provide vendor comparisons.

- Data marketplaces: Snowflake Data Marketplace, AWS Data Exchange, and Databricks Marketplace enable data providers to list and sell datasets. Consider whether a marketplace or direct licensing fits your go-to-market.

- API platforms: Postman, RapidAPI, and Apigee offer API management and developer portals. Stripe, Twilio, and Plaid provide embedded finance and API infrastructure.

- Embedded finance providers: Stripe Connect, Adyen for Platforms, Marqeta, and Finix serve different segments (SMB vs. enterprise, domestic vs. global).

Vendor selection criteria: For cloud cost management, evaluate FOCUS (FinOps Open Cost and Usage Specification) support, multicloud visibility, right-sizing and reservation recommendations, and integration with existing DevOps tooling. For data monetization, assess data governance capabilities, anonymization tools, and compliance workflows. For API products, consider developer experience (documentation, SDKs, sandbox), rate limiting and usage metering, and support for usage-based billing. For embedded finance, compare revenue share models (net vs. gross), onboarding speed, geographic coverage, and support for your vertical (retail, SaaS, healthcare, etc.). Request reference customers and ROI case studies before committing.

Limitations & Critical Perspective

Infrastructure monetization delivers measurable results, but several caveats apply:

- Not every business has monetizable data: Data products require unique, high-quality, anonymizable assets. Commodity data has limited value.

- API products require product mindset: Building and maintaining a developer-friendly API, documentation, and support is a significant investment. Many internal APIs are not suitable for external commercialization.

- Embedded finance is heavily regulated: Payment processing, lending, and insurance require compliance with state and federal regulations. Most SMBs partner with regulated PayFacs rather than becoming PayFacs themselves.

- Cloud savings are not guaranteed: McKinsey’s 15–25% and industry 25–30% figures apply to organizations that implement structured FinOps; results vary by maturity, governance, and workload mix.

- Channel conflict: Monetizing APIs or data that overlap with existing partner or customer relationships can create conflict. Clear boundaries and partner communication are essential.

- Implementation timelines: Cloud optimization can yield results in 3–6 months; data products and API businesses typically require 6–18 months to reach meaningful revenue. Embedded finance pilots may take 12–24 months including regulatory and partner onboarding.

Not every business has monetizable infrastructure. Start with an honest assessment: Do you have unique data? Internal APIs with external demand? Sufficient transaction volume for embedded finance? Cloud optimization is the lowest-risk starting point—savings flow to margin regardless of market demand.

Methodology: How We Researched This Article

We evaluated IT infrastructure monetization using primary and secondary sources:

- Primary: McKinsey (cloud economics, FinOps), Gartner (CFM Magic Quadrant), Forrester (Cloud Cost Management Wave), IDC (data monetization), HBR (infrastructure value, data monetization), BCG (cloud waste, embedded finance), AWS (rightsizing, RIs), Adyen (embedded finance report), Plaid (embedded finance, lending, insurance).

- Industry: Byteiota (cloud waste), Unanswered.io (IT spend benchmarks), B2B Ecosystem (data monetization models), Venable/JD Supra (data licensing), Moesif/Zwitch/Monetizely (API pricing), Usio (embedded payments), Channeltivity (channel conflict).

- Vendor: Mapbox, MapQuest, Rainforest Pay, Stripe, Embed.co.

Sources consulted (40+): McKinsey, Gartner, Forrester, IDC, HBR, BCG, AWS, Adyen, Plaid, Byteiota, Unanswered.io, B2B Ecosystem, Venable, JD Supra, Merritt Law, Moesif, Zwitch, Monetizely, Digital API, Zuplo, Zibly, Usio, Rainforest Pay, SwipeSum, Embed.co, OctoBytes, Forbes, Umbrex, Swagger, Channeltivity, Pedowitz Group, Kiflo, PartnerPortal, Flexera, Apptio, Anglepoint, Mapbox, MapQuest, Michelin/Datarade, PTV Logistics, WIGeoGIS, PayPal Newsroom, Medium/QuarkAndCode, LES International.

Frequently Asked Questions

Can small businesses monetize data without violating privacy?

Yes. Small businesses can monetize anonymized, aggregated data—benchmark reports, industry trends, or usage insights—provided they obtain proper consent where required, comply with GDPR/CCPA, and use data licensing agreements that specify permitted uses. Data must be truly anonymized (not re-identifiable) for many use cases. Consult legal counsel before commercializing data.

What skills do I need to build an API product?

API product development requires product management (defining value proposition, pricing, roadmap), software engineering (designing RESTful or GraphQL APIs, authentication, rate limiting), developer experience (documentation, SDKs, sandbox), and go-to-market (developer relations, partnerships). Many teams start by productizing an internal API with a thin external layer and usage-based pricing.

How do I price infrastructure-derived offerings?

For data products: subscription (monthly/annual access), usage-based (per query or record), or one-time licensing. For APIs: usage-based (per call) is dominant; tiered subscriptions with usage limits are common. For embedded finance: revenue share (percentage of processing fees) or flat fee per transaction. Benchmark competitors and validate willingness-to-pay with potential customers.

What is FinOps and how does it convert savings to profit?

FinOps is a cultural practice and set of tools for cloud financial management—tagging, cost allocation, right-sizing, reserved capacity, and governance. Savings from FinOps flow directly to operating margin. McKinsey estimates 15–25% cost reduction potential; mature programs achieve 25–30% savings. Those savings are equivalent to new profit since they reduce expense without reducing output.

What are the main risks of embedded finance?

Regulatory compliance (money transmission, lending, insurance licensing), partner dependency (relying on PayFac or lender for underwriting and operations), and customer experience (payment failures, disputes). Most platforms partner with regulated providers (Stripe, Adyen, Plaid, Rainforest) rather than becoming regulated entities themselves.

How much can I save with cloud cost optimization?

McKinsey estimates 15–25% cost reduction; mature FinOps programs achieve 25–30% savings. Industry analysis indicates organizations waste 27–32% of cloud budgets—structured FinOps can reduce waste to 15–25%. Savings depend on current maturity, tagging discipline, workload mix, and commitment to governance. Right-sizing and reserved instances can deliver up to 75% discounts vs. on-demand for steady-state workloads.

What is the Infrastructure Monetization Opportunity Assessment?

An assessment framework to inventory monetizable assets (data, APIs, cloud spend), validate demand with potential customers, and prioritize initiatives by revenue potential and implementation complexity. Key questions: What unique data do we have? What internal APIs could be productized? Where is cloud waste? Who would pay for our assets? Conduct discovery interviews, size the market, and build a roadmap with phased MVPs.

How do I price infrastructure-derived offerings?

Cloud optimization savings are internal—no pricing needed; savings flow to margin. Data products: benchmark reports and anonymized insights typically use subscription ($500–$5,000/month) or per-report ($2,000–$15,000) models; licensing fees depend on exclusivity and volume. APIs: usage-based (per call, per record) or tiered subscriptions; align with competitor benchmarks and value delivered. Embedded finance: revenue share (0.3–0.5% of GMV) or per-transaction fees from PayFac partners. Validate pricing with 5–10 potential customers before launch.

Bottom Line: From Cost Center to Profit Driver

U.S. businesses can transform IT infrastructure from an expense line into a profit center through cloud cost optimization (15–25% savings → margin), data monetization (anonymized insights, benchmarks, licensing), the API economy (packaging internal capabilities as paid APIs), and embedded finance (payment processing, lending, insurance revenue share). The average business spends 4–6% of revenue on IT; capturing 2–4% back through savings and new revenue is achievable for organizations that assess assets, validate demand, build MVPs, and scale with appropriate risk management.

Success requires executive sponsorship, cross-functional collaboration (IT, finance, legal, product), and patience—data products and API businesses typically take 6–18 months to reach meaningful revenue. Start with cloud optimization for quick wins, then evaluate data and API opportunities based on your unique assets.

Infrastructure Monetization Opportunity Assessment—practical next steps: (1) Schedule a half-day workshop with IT, finance, and business leaders to inventory monetizable assets. (2) For cloud: Run a 30-day Cost Explorer or equivalent analysis; identify top 10 waste categories; assign owners for tagging and right-sizing. (3) For data: List datasets (customer, operational, market); assess anonymization feasibility; identify 3–5 potential customer segments. (4) For APIs: Catalog internal services with external demand potential; estimate development effort to productize; validate with 5–10 potential customers. (5) For embedded finance: Assess current payment flow; model revenue at 0.3–0.5% of GMV; evaluate Stripe Connect, Adyen, or Plaid integration. (6) Prioritize initiatives by revenue potential × implementation feasibility; build 90-day roadmap with clear milestones. A business model canvas template can help structure the assessment—downloadable from strategy consulting firms or business development resources.

Technology profit centers—the CFO view: Organizations that monetize technology spend 8.54% of revenue on IT versus 3.66% for those that do not, per Unanswered.io—suggesting that strategic infrastructure investment, when coupled with monetization, generates returns beyond cost savings. Industry benchmarks by sector: technology/software firms 18%, financial services 4.4–11.4%, manufacturing 1.4–3.2%, consumer goods 2–3%. Small businesses (under $50M revenue) average 4–6%; mid-sized ($50M–$1B) 3%; large enterprises (over $1B) 2%. The key is not spending less—it is ensuring every dollar spent either reduces cost (FinOps) or generates revenue (data, APIs, embedded finance).

Next steps:

- Conduct an infrastructure monetization assessment — Inventory data, API capabilities, and cloud spend.

- Prioritize quick wins — Implement FinOps practices; target 15–25% cloud cost reduction.

- Validate data and API opportunities — Interview potential customers; size the market.

- Pilot with low-risk MVPs — Benchmark report, limited API access, or embedded payment pilot.

CTA: Infrastructure Monetization Opportunity Assessment

Business owners and executives evaluating technology ROI can use this article as a framework for an Infrastructure Monetization Opportunity Assessment. Key deliverables: (1) Asset inventory—data, APIs, cloud spend; (2) Demand validation—customer interviews, market sizing; (3) Prioritized roadmap—quick wins (FinOps) and longer-term initiatives (data, API, embedded finance); (4) Risk register—compliance, channel conflict, implementation complexity. Strategy consultants and technology advisors often offer assessment workshops; alternatively, internal cross-functional teams can conduct a self-assessment using the business model canvas and phased implementation framework outlined in Section 5. Downloadable templates for business model canvas and opportunity assessment are available from business development and strategy resources.

Resources:

→ McKinsey — More for Less: Five Ways to Lower Cloud Costs

→ Gartner — Cloud Financial Management Tools

→ HBR — Capture New Value from Your Existing Tech Infrastructure

→ Adyen/BCG — Embedded Finance Report

→ Plaid — What is Embedded Finance?

→ FinOps Foundation — Best Practices

Information as of March 2026. Vendor offerings, regulations, and market conditions change frequently. Verify details with providers and legal counsel before making investment decisions.